Why Indexed Universal Life Insurance Beats Traditional Retirement Plans

The Problem: Generic Advice and Hidden Fees

If you’ve ever walked out of a financial advisor’s office feeling more confused than when you walked in, you’re not alone. Too many families are handed a pamphlet, asked about “risk tolerance,” and told to “trust the market.” Generic advice. High fees. No real strategy.

People want more than a cookie-cutter investment plan—they want clarity, control, and confidence in their financial future. Unfortunately, traditional advisors are often trained to sell products, not solve problems. That’s where Indexed Universal Life Insurance (IUL) changes the game.

401(k) vs. Indexed Universal Life Insurance: A Smarter Comparison

When it comes to building wealth, most people are told, “Just put your money in a 401(k) and forget about it.” But the truth is, a 401(k) has several limitations that can quietly eat away at your future income.

1. Market Risk and Volatility

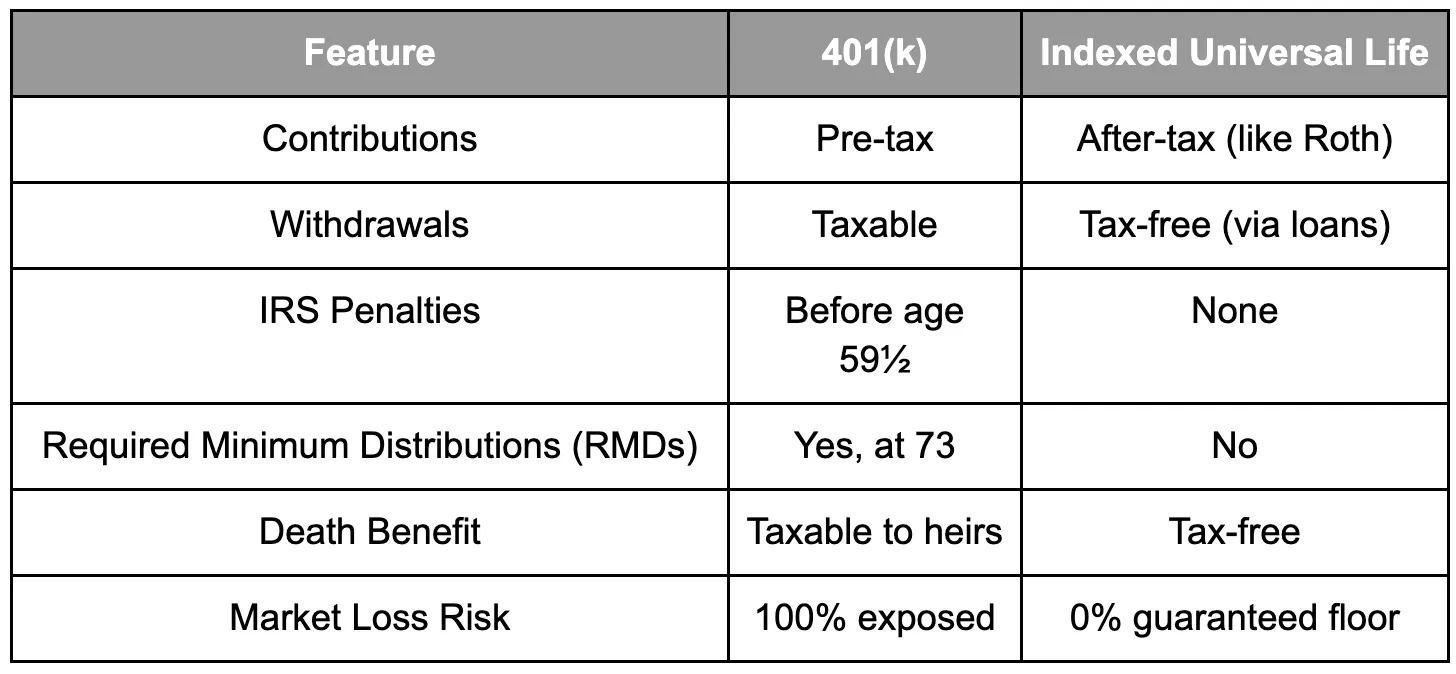

A 401(k) is directly tied to the ups and downs of the stock market. When the market drops, so does your account. You bear all the risk, while your advisor still collects fees.

An IUL, however, links your returns to a market index—such as the S&P 500—without actually investing your money in it. That means when the market rises, your account participates in the gains (up to a cap), but when it falls, your principal is protected from loss.

2. Taxation and Retirement Withdrawals

Your 401(k) grows tax-deferred—but the key word there is deferred, not free. Every dollar you withdraw in retirement is taxed as ordinary income, potentially pushing you into a higher tax bracket later in life.

With an IUL, your money can grow tax-advantaged, and you can access it tax-free through policy loans or withdrawals against your cash value. The IRS doesn’t view policy loans as income—making this one of the most powerful wealth-building strategies available.

3. Liquidity and Flexibility

Most people can’t touch their 401(k) funds before age 59½ without facing penalties. Life doesn’t always wait that long.

An IUL allows you to access your money at any time—for opportunities, emergencies, or supplemental income—without IRS penalties or restrictions.

4. Beneficiary Protection

A 401(k) is a pure investment account. When you pass away, your heirs inherit what’s left—minus taxes.

An IUL, on the other hand, provides a death benefit that passes income-tax free to your beneficiaries, ensuring your family is protected no matter what happens.

401(k) vs. Indexed Universal Life: The Truth About Fees

When comparing investment tools, most people only look at returns—but fees quietly determine how much you actually keep. Understanding how 401(k) fees stack up against those of an Indexed Universal Life (IUL) policy reveals why so many families are making the switch.

The Hidden Costs of a 401(k)

A typical 401(k) plan comes with multiple layers of fees—many of which are rarely explained clearly to the investor. These can include:

- Administrative Fees: Record keeping, custodial, and compliance costs that can run 0.25–0.50% annually.

- Investment Management Fees: Fund managers charge anywhere from 0.5–1.5% to oversee your chosen mutual funds.

- Advisory Fees: Many financial advisors add another 1% or more for “management.”

- Trading Costs and Expense Ratios: Every shift in portfolio allocation comes with additional internal fund expenses.

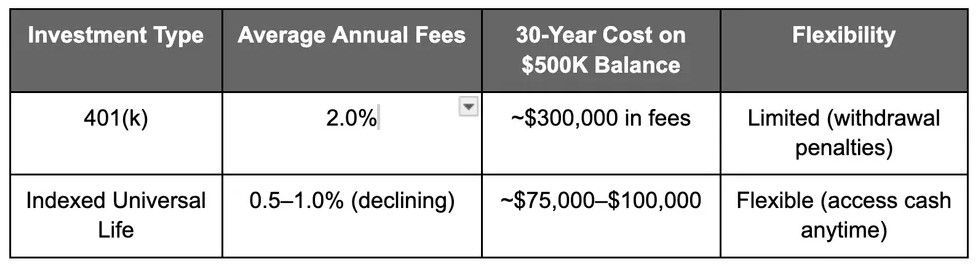

In total, it’s common for 401(k) participants to lose 1.5%–3% per year to fees—whether their account performs well or not. Over a 30-year career, that can easily cost hundreds of thousands of dollars in lost growth.

And here’s the real sting: 401(k) fees are charged on your total balance. Even when your account loses value in a down market, the fees keep coming out.

The Transparent Fee Structure of an IUL

With an Indexed Universal Life policy, the costs are structured differently—and far more transparent.

Here’s what you can expect:

- Cost of Insurance (COI): Covers the actual life insurance protection and decreases as your cash value grows.

- Policy Fees: Small administrative charges, typically fixed or declining over time.

- Index Participation Limits: Instead of ongoing fund fees, your growth is tied to index performance with caps and participation rates—meaning no hidden management fees.

Unlike 401(k)s, there are no advisory or fund management fees, and no annual percentage charged on your total balance. Once the front-end insurance costs are covered, your cash value compounds within the policy without continual deductions.

Over time, the IUL’s internal costs often drop to well below 1%, while your 401(k) can continue draining 2–3% annually forever.

Lifetime Fee Impact Example

In Simple Terms:

✅ The IUL’s front-loaded costs taper off as your cash value grows.

🚫 The 401(k)’s compounding fees keep eating into your balance forever.

The Bottom Line on Fees

While no financial vehicle is “free,” an IUL’s transparent, declining cost structure puts more of your money to work for you—without hidden fund charges or advisor commissions draining your returns. Add the tax advantages and risk protection, and the IUL becomes a clear winner for anyone serious about long-term wealth growth.

Myths vs. Facts About Indexed Universal Life Insurance

Let’s address some of the most common misconceptions you’ll hear from those who don’t fully understand how modern IULs work.

Myth #1: “IULs are expensive.”

Fact: Every financial product has costs. But when you compare the total fees—administrative costs, fund expenses, and advisor fees—an IUL often comes out lower than a 401(k). In a 401(k), you could easily pay 1–2% or more annually in hidden fees, even when the market performs poorly.

With an IUL, fees are transparent and front-loaded, meaning they reduce over time as your cash value grows.

Myth #2: “Premiums go up in an IUL.”

Fact: Not true. Your cost of insurance is level or predictable depending on the product design. You can adjust your contributions, skip payments if your cash value is strong, and still maintain coverage. The flexibility of an IUL is one of its greatest advantages.

Myth #3: “IULs are risky because they’re tied to the stock market.”

Fact: This is where most people misunderstand the “indexed” part. Your IUL’s growth is linked to an index, not invested in it. That means you benefit when the index goes up, but you never lose when it goes down. Your worst-case scenario is a 0% return—not a loss of principal.

Myth #4: “401(k)s have better tax benefits.”

Fact: 401(k)s delay taxes—they don’t eliminate them. In contrast, IULs let your money grow tax-deferred and be accessed tax-free later. That’s a true tax-advantaged strategy—especially powerful when taxes are likely to rise in the future.

Why Indexed Universal Life Insurance Is a Safer, Smarter Investment Vehicle

1. No-Risk Structure

In an IUL, your cash value is never at risk from market downturns. Insurance companies guarantee a floor rate of 0% (some even slightly higher). You can only go up, never down. This creates peace of mind that traditional investments simply can’t match.

2. Solid Return Potential

IUL returns are based on the performance of your chosen index. When the S&P 500 or Nasdaq performs well, your policy can earn a competitive rate of return, typically ranging from 6–9% average over time, depending on caps and participation rates. Over decades, this growth—without market losses—can dramatically outperform volatile 401(k) results.

3. Flexibility Across Life Stages

Life changes. Your savings plan should adapt with you. You can increase, decrease, or pause your IUL premiums depending on your financial situation. Try calling your 401(k) manager and asking for that kind of flexibility—it doesn’t exist.

4. Tax-Free Legacy and Living Benefits

Unlike traditional investment vehicles, modern IULs include living benefits—allowing you to access your death benefit in the event of a chronic, critical, or terminal illness. That means your policy not only grows wealth but also protects you while you’re alive.

5. Peace of Mind in Every Market

In uncertain times—whether due to inflation, interest-rate changes, or global market volatility—an IUL can be a safe harbor. You can sleep at night knowing your account will never lose value due to market crashes.

The Tax Advantages That Outperform a 401(k)

One of the most overlooked advantages of an IUL is how it shields your money from future tax hikes. Here’s how it stacks up:

In short, IULs combine the best of both worlds: growth potential + protection. And unlike a 401(k), you’re not forced to take distributions or pay taxes on gains you never actually “sold.”

The Real Cost of “Free Advice”

Many advisors promote 401(k)s and mutual funds because that’s where they earn their recurring fees—usually a percentage of your assets under management. The more you invest, the more they make, even if you lose money.

At Russell Financial Solutions, our mission is different. We educate clients on how money actually works—how to build tax-free wealth, create guaranteed income, and protect your family at the same time. We don’t charge hidden fees, and we don’t sell one-size-fits-all solutions. We teach you how to make smart money moves that align with your life, not someone else’s commission check.

Ready to Reimagine Your Retirement?

Traditional retirement plans were built for a world that no longer exists. Today, flexibility, tax efficiency, and protection are just as important as growth.

Indexed Universal Life Insurance isn’t just another product. It’s a modern strategy for real people who want to take control of their financial future.

📞 Contact Russell Financial Solutions today to explore whether an Indexed Universal Life policy is right for you.

Thomas: 727-439-6137

Jennifer: 727-249-3339

Thomas@RussellFinancialSolutions.com

Jennifer@RussellFinancialSolutions.com

We’ll walk you through the numbers, explain how your money grows, and design a custom plan that fits your goals.

Because your financial future deserves more than a pamphlet, it deserves a plan.